Checking for Errors on Your Credit Report: A Step-by-Step Guide for Canadians

Published on June 17, 2025 | By WealthFusions Finance Team

Your credit report plays a critical role in your financial life, affecting everything from loan approvals to interest rates. Yet, errors on your report can unfairly damage your credit score. This guide will walk you through how to check your credit report for errors, understand common mistakes, and take the right steps to fix them quickly. Protect your credit and your financial future with confidence.

1. Obtain Your Free Credit Reports from Canada’s Two Major Bureaus

In Canada, two credit bureaus maintain your credit files: Equifax Canada and TransUnion Canada. Under federal law, you can request a free credit report once per year from each bureau.

Tip: Get reports from both bureaus as they sometimes contain slightly different data.

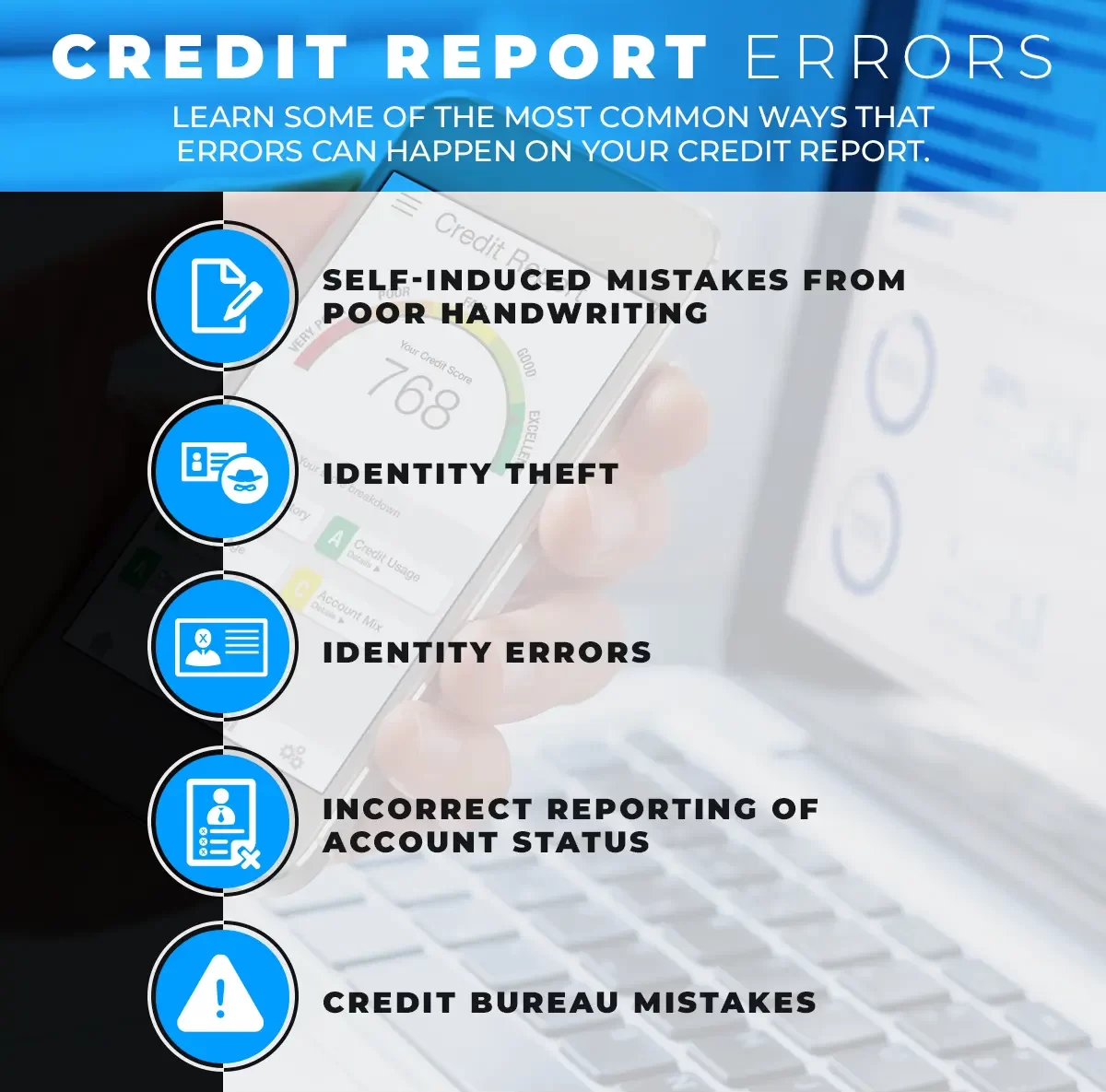

2. Understand Common Credit Report Errors

Errors can appear in several forms:

- Personal Information Mistakes: Wrong name, address, or date of birth.

- Accounts That Don’t Belong to You: Fraudulent or outdated accounts.

- Incorrect Payment History: Missed payments wrongly reported.

- Duplicate Accounts: Same account listed multiple times.

- Closed Accounts Reported as Open: Can lower your credit score.

According to a 2023 FTC report, about 20% of consumers find errors that could hurt their credit.

3. Review Your Credit Report Thoroughly

Set aside time (about 30-45 minutes) to carefully review each section of your report:

- Personal Information: Verify names, addresses, and Social Insurance Number (SIN) matches.

- Credit Accounts: Confirm account types, balances, and payment histories are accurate.

- Enquiries: Look for unauthorized or suspicious credit checks.

- Public Records: Check for bankruptcies or judgments you don’t recognize.

4. Document Errors with Evidence

If you spot inaccuracies, gather supporting documents like:

- Bank statements

- Payment receipts

- Correspondence from lenders

- Identity proof

This evidence strengthens your dispute case with the credit bureau.

5. Dispute Errors with the Credit Bureau

Both Equifax and TransUnion allow online, phone, or mail disputes. Your dispute letter should include:

- Your full name, address, and date of birth

- Identification number on the credit report

- Clear description of each error

- Copies (never originals) of supporting documents

- Request to correct or remove the erroneous information

Example Dispute Template:

“I am writing to dispute the following errors on my credit report. Account number 12345 is incorrectly reported as delinquent. Enclosed are payment receipts proving timely payments. Please investigate and correct this error as soon as possible.”

6. Follow Up and Monitor Results

Credit bureaus have 30 days to investigate. They contact the creditor to verify your claim. You will receive a written report with results.

If the error is confirmed, the bureau will update your report and notify you. If rejected, you can add a consumer statement explaining your side.

Tip: Regularly monitor your credit report every 6-12 months to catch errors early.

7. Protect Yourself from Fraud and Identity Theft

Errors can be signs of identity theft. Take these precautions:

- Sign up for credit monitoring services

- Place a fraud alert or credit freeze if suspicious activity arises

- Review your credit card and bank statements monthly

8. Know Your Rights and When to Seek Help

Under Canada’s Personal Information Protection and Electronic Documents Act (PIPEDA), you have the right to access and correct your credit information.

If disputes become complex, consider consulting a credit counselor or legal expert specializing in consumer rights.

Summary & Next Steps

Regularly checking your credit report for errors is a vital part of maintaining a healthy credit score in Canada. Obtain your free reports annually, review all details carefully, dispute inaccuracies promptly, and monitor ongoing changes. These proactive steps can save you thousands in higher interest rates and denied credit.

Visit for help reviewing your credit report and improving your financial health.

Frequently Asked Questions

- 1. How often can I get a free credit report in Canada?

- You can request a free copy once a year from each of Equifax and TransUnion.

- 2. How long does a credit dispute take?

- Credit bureaus generally resolve disputes within 30 days.

- 3. Will fixing errors improve my credit score immediately?

- Once corrected, your credit score can improve within 1-2 reporting cycles (30-60 days).

- 4. Can I dispute an error online?

- Yes, both Equifax and TransUnion offer online dispute submission forms.

- 5. What if the creditor denies my dispute?

- You can add a consumer statement explaining your position to your credit report.

- 6. How can I protect myself from credit report errors?

- Regularly monitor your reports and use credit monitoring services for alerts.

- 7. Are credit reports the same as credit scores?

- No. A credit report lists your credit history; a credit score is a numerical summary of your creditworthiness.

- 8. Can identity theft cause errors on my credit report?

- Yes. Unauthorized accounts or inquiries can appear as errors due to fraud.