Using Debit Cards in Canada: 2025 Guide to Fees, Limits & Fraud Safety

Updated June 16, 2025 | By WealthFusions Finance Team

Debit cards are one of the most popular ways to pay and manage everyday spending in Canada—whether you’re buying groceries, paying bills, or sending e-Transfers. But many Canadians unknowingly pay hidden fees, exceed transaction limits, or risk fraud by not understanding how their card really works.

In this guide, we break down everything you need to know to use your debit card smarter and safer: from avoiding ATM charges to protecting your PIN, increasing your daily limits, and knowing when to use credit instead.

1. What Is a Debit Card in Canada?

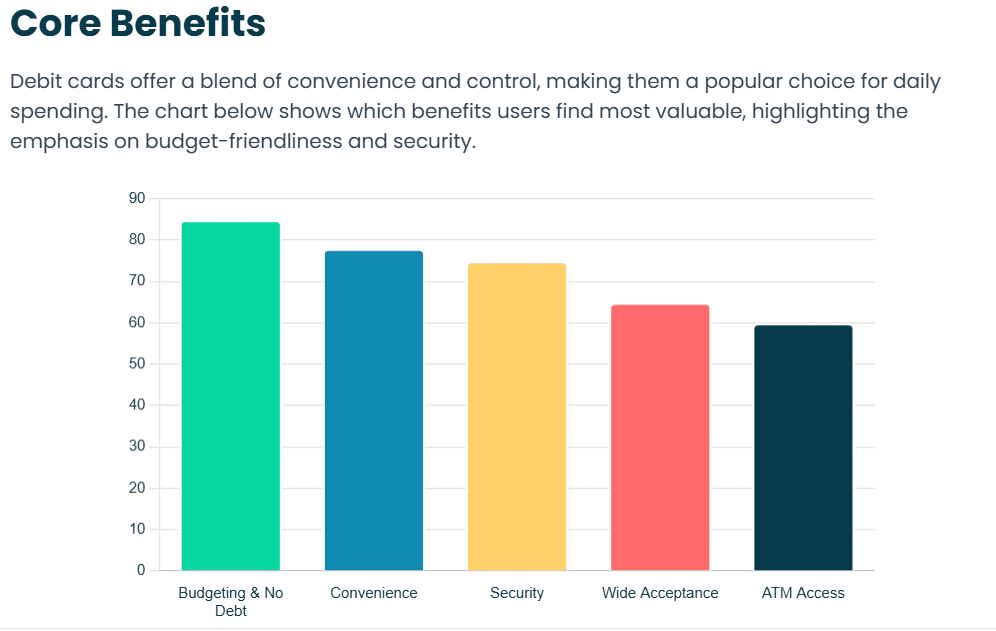

A debit card is a payment card linked directly to your chequing or savings account. It lets you spend only what you already have—no borrowing or interest charges involved.

- Network: Most Canadian debit cards use Interac, Canada’s secure domestic network.

- Functions: Tap-to-pay, online shopping (Canadian sites), ATM withdrawals, and bill payments.

- Mobile use: Most debit cards work with Apple Pay and Google Pay.

Note: If your debit card has a Visa Debit or Mastercard Debit logo, it can be used internationally and at global online retailers.

2. Understand Your Daily Debit Limits

Most banks set daily spending and withdrawal caps to reduce fraud risk. Knowing your limits helps you plan larger purchases and avoid declined transactions.

| Bank | POS Limit | ATM Limit | Changeable Online? |

|---|---|---|---|

| TD Canada Trust | $3,000 | $1,000 | Yes |

| RBC | $2,500 | $1,000 | No |

| Scotiabank | $2,000 | $960 | Yes |

| Simplii Financial | $3,000 | $1,200 | Yes |

Tip: You can usually request a temporary increase for large purchases—such as tuition or appliances—via your bank’s app or call center.

3. Avoid Common Debit Card Fees

While debit card use is often free, many banks charge for out-of-network use, cross-border transactions, or certain e-Transfers.

- ATM fees: $1.50–$3.00 when using a non-network ATM (especially at convenience stores or airports).

- Foreign transaction fees: Typically 2.5–3% if used outside Canada or online at non-Canadian stores.

- Interac e-Transfer fees: Some accounts still charge $1 per transfer if not included in your plan.

Ways to avoid fees:

- Use The EXCHANGE® ATM network (free for many digital banks).

- Choose no-fee chequing accounts like Tangerine, Simplii, or EQ Bank.

- Use a travel credit card for purchases abroad to avoid debit-related FX fees.

4. Stay Safe: Debit Card Security Tips

In 2024, Canadians reported over $112 million in debit and card fraud. Protect yourself with these tips:

- Set real-time alerts: Get notified by text or email for every transaction or unusual login attempt.

- Limit tap-to-pay: Use tap only for small purchases; set your tap limit to $100 or less.

- Lock cards instantly: Lost your card? Use your bank’s app to freeze or cancel it on the spot.

- Monitor activity weekly: Log in regularly to spot and report suspicious transactions quickly.

Reminder: Always cover your PIN when entering it at a terminal. Never write it down or share it.

5. Debit Card vs. Credit Card: Which Should You Use?

| Feature | Debit Card | Credit Card |

|---|---|---|

| Source of Funds | Direct from your bank | Credit limit (pay later) |

| Interest Charges | None | Yes (if balance isn’t paid) |

| Builds Credit Score | No | Yes |

| Fraud Protection | Moderate | Strong (chargebacks available) |

| Rewards/Cashback | Rare | Common |

Bottom Line: Use a debit card for budgeting and day-to-day purchases; use credit for building credit and earning rewards—just pay your balance off each month.

6. What to Do If Your Debit Card Is Lost or Compromised

Act fast if you lose your card or notice fraud:

- Lock your card immediately through your mobile banking app.

- Call your bank’s 24/7 fraud hotline (e.g., TD: 1‑866‑222‑3456, RBC: 1‑800‑769‑2511).

- File a fraud claim. Most banks resolve claims within 10 business days.

Important: You may be liable for losses if you shared your PIN, wrote it down, or delayed reporting fraud.

Final Thoughts: Debit Done Right

Debit cards are powerful tools when used correctly. Stick with your bank’s network, monitor your activity, and learn your account’s limits and features. With smart habits, you’ll avoid fees, stay secure, and make every transaction count.

visit this page? to get updated with the changing situation.

Frequently Asked Questions (FAQ)

- Can I use my Canadian debit card abroad?

- Only if it’s a Visa or Mastercard Debit card. Interac-only cards don’t work internationally.

- What happens if I go over my debit limit?

- The transaction will be declined. If you have overdraft protection, you may be charged interest or a fee.

- Is contactless (tap) safe?

- Yes, especially for small transactions. Set a tap limit and monitor your alerts regularly.

- Are debit card purchases protected?

- Yes, but less so than credit. Look for accounts with zero-liability policies for added protection.

- Can I get cashback with debit?

- Rarely. Some banks (like RBC’s ValuePlus) offer debit rewards, but credit cards typically offer better returns.

- How do I change my daily transaction limit?

- Log in to your bank’s app or call support. Most allow adjustments within your credit profile’s risk parameters.